2023年绿色出行出海趋势第2期:中国汽车品牌出海现状

来源:岭南论坛 时间:2023-07-05

上一期我们提到目前新能源汽车已经成为中国汽车出口的核心增长点,而在电池新能源汽车(BEV)、插电式混合动力新能源汽车(PHEV)、混合动力新能源汽车(HEV)三种新能源车类型中,电池新能源汽车BEV是中国新能源车出海的绝对主力。

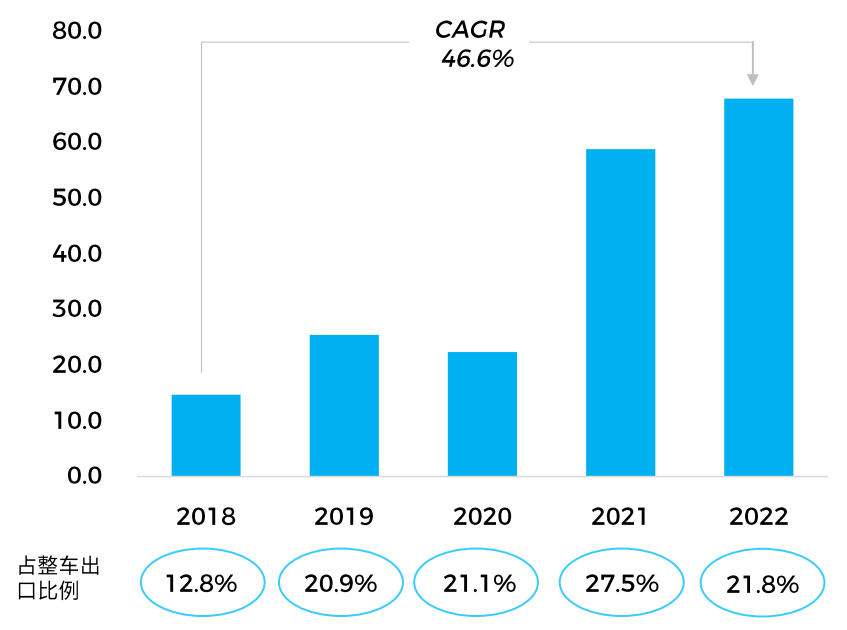

2018-2022中国新能源汽车出口量(单位:万辆)

(图来源:飞书点跃《2023年绿色出行出海趋势报告》,中国汽车工业协会,全国乘用车联合会,Meet Intelligence)

在政策和市场双重推动作用下,2022年中国新能源汽车继续延续2021年增长态势,其中乘用车为新能源出口绝对主力。此外,俄乌冲突助推国际油价迅速攀升并保持高位,叠加各国针对纯电车强补贴政策拉动,加速了中国汽车品牌的出海进程,尤其是中国低价微型纯电动车款备受海外消费者青睐。

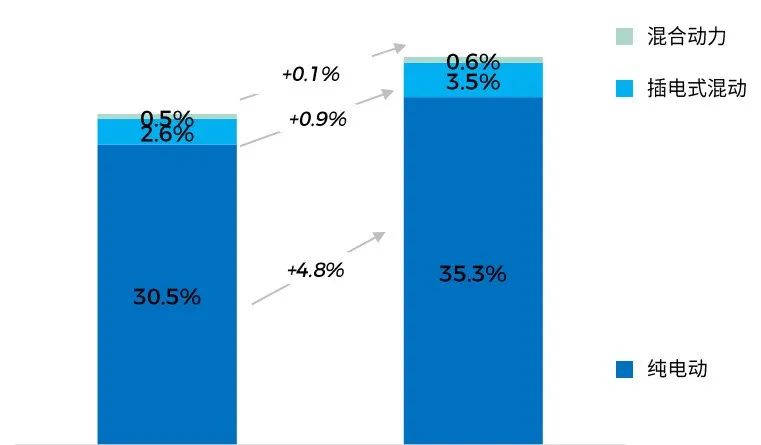

2021、2022年中国新能源汽车出口量(单位:万辆)

(图来源:飞书点跃《2023年绿色出行出海趋势报告》,中国汽车工业协会,全国乘用车联合会,Meet Intelligence)

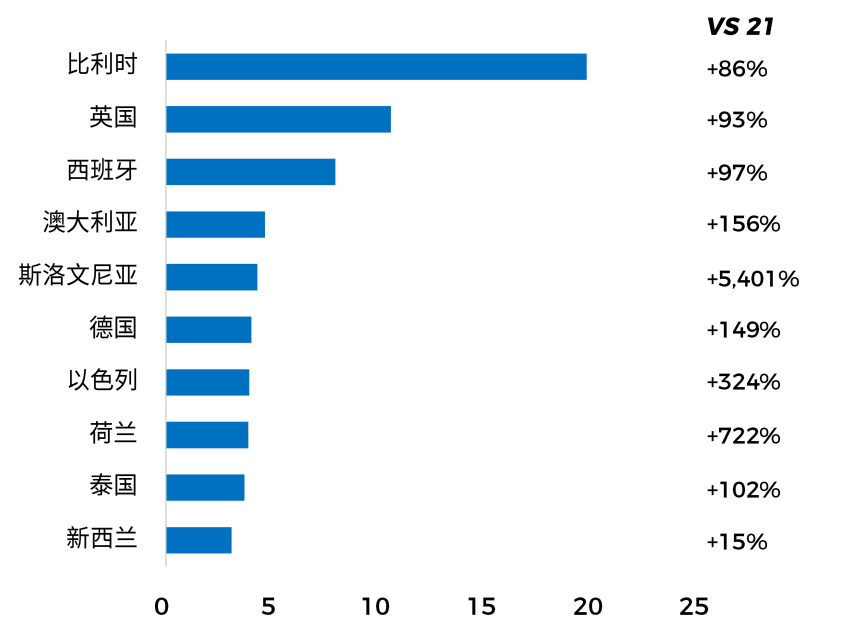

具体到地域上看,中国新能源厂商对西欧国家及部分东南亚地区出口表现最为强劲,成为中国新能源汽车出口的主要增量市场,这是由于全球大部分地区正积极推出购车补贴、低关税、加快充电设施建设等新能源汽车引导政策,各国激进的购车优惠补贴政策为中国新能源汽车出海提供黄金窗口期。

2022年中国新能源汽车Top出口目的国(单位:万辆)

(图来源:飞书点跃《2023年绿色出行出海趋势报告》,中国汽车工业协会,Meet Intelligence)

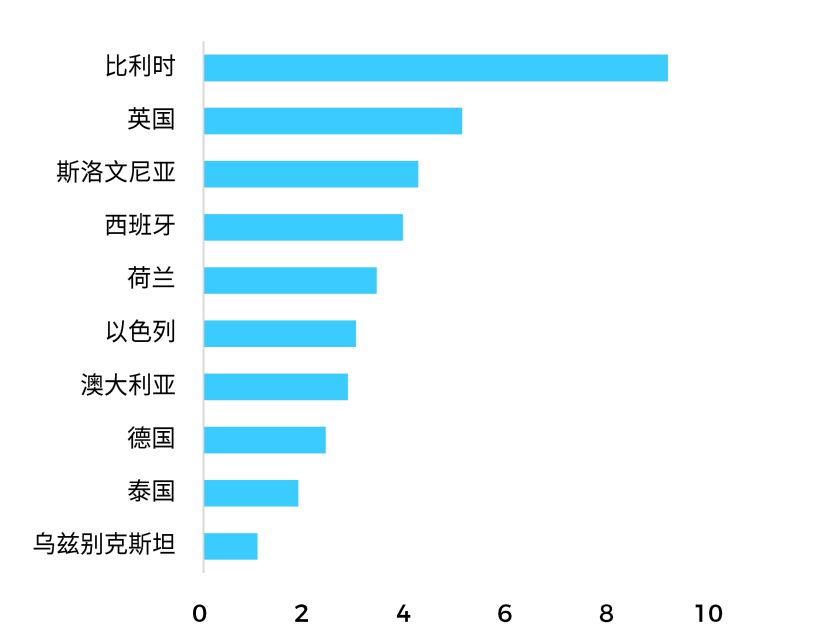

2022年中国新能源汽车出口增长Top增量市场(单位:万辆)

(图来源:飞书点跃《2023年绿色出行出海趋势报告》,中国汽车工业协会,Meet Intelligence)

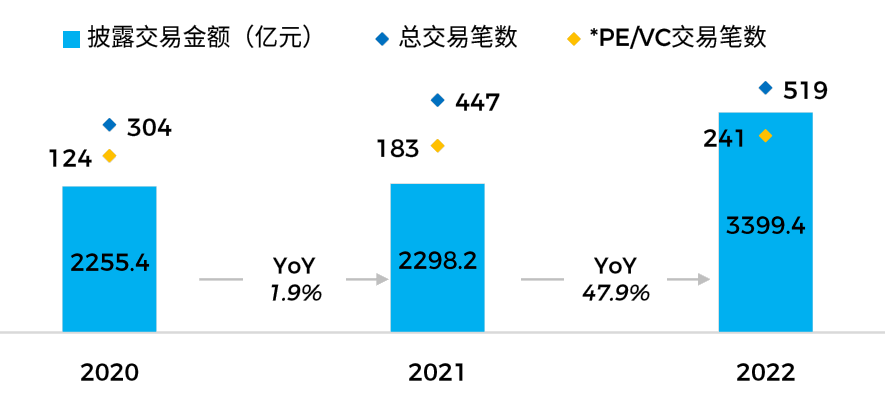

此外,产销及出口增长势头的良好,与资本的大力推动也有关系。“双碳”风潮下,众多资本纷纷加速产业布局新能源汽车,掀起投资热潮。

2020-2022中国新能源行业投资并购总览

(图来源:飞书点跃《2023年绿色出行出海趋势报告》,Cvsource,Meet Intelligence)

从投资项目看,部分资本投向了由广汽、长安、吉利等传统车企孵化的新能源整车项目,部分则流向了造车新势力。造车新势力中,蔚来、小鹏、零跑、哪吒背后资本阵容最为庞大,除哪吒外,其余三家已成功上市,且在市场上形成了一定的品牌影响。

2021-2022中国新能源汽车赛道Top融资项目

(图来源:飞书点跃《2023年绿色出行出海趋势报告》,Cvsource,Meet Intelligence)

总的来说,技术进步、供应链规模以及海外政策利好是中国新能源汽车出海的三大驱动力。

目前,中国新能源整车造车技术基本达到国际先进水平,具体来说,包括从产品外观、内饰、续航里程、环境适应性到整车性能、质量、能耗、智能化应用等方面,在国际市场上都具备竞争优势,受到海外用户认可。

中国新能源汽车生产供应链的完备性和规模化,有力地支撑了国内车企新能源整车的出口。尤其是新能源汽车供应链中的汽车动力电池,国内的动力电池技术已达到国际领先水平,单体能量密度持续提升,且产能主要分布在中国。除动力电池外,新能源车的驱动电机技术基本与国外技术同步,电控关键技术已基本掌握并实现国产化。

包括欧洲在内的多国政府加大对新能源汽车的补贴力度,激发了人们的购车意愿,全球电动车市场快速扩张,为中国新能源汽车出口提供了黄金机遇。

目前,中国新能源车企出海较为成功的品牌包括比亚迪、蔚来、小鹏、长城、奇瑞、吉利、上汽名爵等。

以比亚迪为例,其主要出海国家为荷兰、挪威和德国等70多个国家和地区,是目前国内新能源车企中出海地域最广的车企,主要出口车型为轿车、SUV,主要产品包括唐EV、宋plus DM-i、元PLUS等王朝系列,海豚和海豹等多款,其价格区间在21-72万元。比亚迪的产品主要卖点是其基于纯电技术平台e3.0、DM-i超级混动技术、“刀片电池”技术等打造的新能源汽车领先的技术水平,以及包括旋转Pad导航界面、前卫用色的设计外形。比亚迪的经营模式包括与欧洲汽车经销商Louwman合作以获取当地销售渠道,在泰国、印度建厂增强全球供应能力等。

以蔚来为例,其主要出海国家为挪威、德国、荷兰、丹麦、瑞典等,主要出口车型为SUV,主要产品包括EL7、ES8、ET7,价格区间在45万元起,产品主要卖点包括以自动驾驶技术、车电分离为核心的高智能和高性能,,其经营模式为直营+订阅,并在匈牙利建设蔚来能源欧洲工厂。

以小鹏为例,其主要出海国家为荷兰、瑞典、挪威、丹麦,主要出口车型为轿车、SUV,主要产品包括P5、P7、G9,价格区间在28-37.7万元,产品主要卖点包括整车流线型设计,科技简约内饰设计,长续航、超级快充,智能辅助驾驶系统、智能舒适/睡眠/娱乐空间等智能化体验,经营模式为直营+授权经销。

以长城为例,其主要出海国家为东南亚、英国、南非等国家和地区,主要出口车型为SUV,主要产品包括欧拉、哈弗、坦克,价格区间在14-23万元,以物美价廉为产品主要卖点经营模式包括与汽车零售商英之杰集团合作,并在俄罗斯、巴西、泰国自建厂。

可以看出,不同车企之间,产品系列、产品卖点和营销体系等出海模式均有所区别,对应的目标市场也有所不同,在技术革新和灵活经营模式下,中国新能源品牌正加速布局海外市场,抢占海外新能源汽车不同细分领域市场份额。

下一期,我们将介绍海外新能源车市场总体情况,并按地域逐个市场展开讨论。

(本文内容为笔者对飞书点跃《2023年绿色出行出海趋势报告:新能源汽车和E-bike市场解读》报告的部分摘录以及笔者阅读过程中的个人观点,欢迎大家批评指正。)